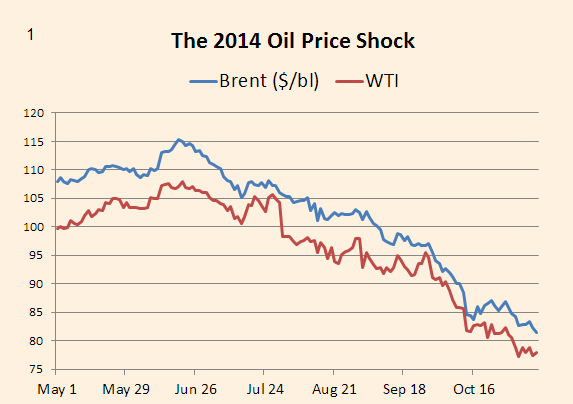

The most significant economic shock in the global economy so far in 2014 has been the drop of more than 25 per cent in spot oil prices since the end of June. Since this shock is attributed by most energy analysts to an increase in oil supply, and not to a decline in global oil demand, this should have led to a significant decline in near-term world inflation forecasts, and to upgrades in global economic growth forecasts.

The most significant economic shock in the global economy so far in 2014 has been the drop of more than 25 per cent in spot oil prices since the end of June. Since this shock is attributed by most energy analysts to an increase in oil supply, and not to a decline in global oil demand, this should have led to a significant decline in near-term world inflation forecasts, and to upgrades in global economic growth forecasts.

The disinflationary effects are uncontroversial. Lower oil prices have obvious direct and indirect effects on consumer prices. But the boost to growth is more debatable, since lower oil prices involve a redistribution of income from oil producers to oil consumers. Why should this reallocation of resources lead to a rise in real gross domestic product?

It is because of time lags. Oil consumers, which are mainly households, have seen their real incomes rise, perhaps permanently, and they are assumed to allocate part of this gain quite quickly to increased real expenditure on other goods and services. Oil producers, on the other hand, are mainly rich governments and corporates, and they may take much longer to reduce their expenditure in line with their lower real incomes.

That, anyway, is what economic models tend to assume when oil prices decline for supply-related reasons. However, as Bruce Kasman of JPMorgan Chase pointed out to me in a conversation yesterday, this is not what has actually happened since the 2014 oil shock occurred. Inflation forecasts have been revised down as expected, but GDP growth projections have also been revised downwards, not upwards. What is this telling us?

First, let us take a look at the numbers. A standard macroeconomic simulation of the effects of a large change in oil prices was published recently by the International Monetary Fund. This is similar to (or slightly smaller than) the shock that has just occurred [1], and persists for several years. This is what the simulations show:

The level of global real GDP in graph 2 is boosted after one year by about 0.5-1.2 per cent, depending on whether we take account only of the fairly direct effects on income distribution mentioned above (red line), or whether we add in the boost to economic and market confidence that may also be involved (blue line). The boost to the level of GDP lasts for about two years before starting to decline. Meanwhile, the 12-month rate of price inflation in graph 3 falls by between 0.5 per cent and 0.9 per cent in the first year, and is then slightly higher in subsequent years.

The exact size of these effects varies considerably in different economic models, but the broad direction is fairly standard. Since almost no economic forecasters had anticipated the recent decline in oil prices in advance, we would expect to see these changes reflected in forecast revisions since the oil shock started in June. But this is not what we have actually observed:

Graphs 4 and 5 show how consensus economic forecasts for inflation and real GDP growth have evolved since the beginning of this year. The green lines show how forecasts for calendar 2014 have been changed through time, while the blue lines show how projections for calendar 2015 have altered.

The decline in inflation projections in the advanced economies since the oil shock is about 0.1 per cent in 2014, and 0.3 per cent in 2015, implying that the level of prices in 2015 will be about 0.4 per cent below the level anticipated by forecasters prior to the oil shock. This is on the low end of the range suggested by the IMF simulations for 2015, but at least it is in the right direction, and is broadly of the right sort of magnitude.

However, the real GDP growth projections for the advanced economies have been revised downwards, by about 0.2 per cent in 2014 and by a further 0.2 per cent in 2015, implying that the level of real GDP will be about 0.4 per cent below the level anticipated before the oil shock. This is in totally the opposite direction to what is shown in the IMF simulations [2].

There are several possible explanations for this [3], but the most likely is that economists have built in the effects of a second economic shock, which they believe will more than offset the beneficial effects of the oil shock on global growth rates. The most obvious such shock is the slowdown in growth in the eurozone, along with the apparently rising probability that the euro economy will get mired in a prolonged period of deflation. Another possible shock is the hard landing that is underway in the property sector in China, which may drag the rest of the Chinese economy down with it.

There is, however, one problem with this explanation. When we examine “nowcasts” of economic activity for the global economy in recent months, we do not see any evidence that the growth rate is slowing down. There has been some slowdown in the eurozone, but this is offset by a rise in the growth rate in the US, while China has been fairly stable.

Therefore the slowdown in global growth in calendar years 2014 and 2015 shown in graph 5 is, so far, entirely in the realm of a forecast, rather than in actual hard economic data. There has, admittedly, been some drop in business surveys in the services sector in recent months, but this is from very elevated levels, and these surveys remain consistent with recent GDP growth rates.

Therefore the slowdown in global growth in calendar years 2014 and 2015 shown in graph 5 is, so far, entirely in the realm of a forecast, rather than in actual hard economic data. There has, admittedly, been some drop in business surveys in the services sector in recent months, but this is from very elevated levels, and these surveys remain consistent with recent GDP growth rates.

An alternative conclusion is that economists have been under-estimating the beneficial effects on GDP growth that will be felt in the next few months from the oil shock, assuming that oil prices stay at or below present levels for a while. Many oil analysts now seem to think that this will be the case, with a common view being that prices will drop below $75 a barrel before the end of the year, and then rebound only slightly next year. But they have been strangely reluctant to revise their official GDP forecasts upwards as a result.

If that view proves right, global GDP forecasts may be revised upwards in coming months, dissipating some of the gloom that currently surrounds the immediate future for the global economy.

——————————————————————————————————

Notes

[1] The published IMF simulation actually shows the impact of an upward shock to oil prices triggered by a drop in Iraqi oil output. I have changed all the signs here. This is not perfect by any means (notably, policy responses may not be equivalent in both directions), but the effects simulated by the models are likely to be roughly symmetrical. Many other simulations are broadly similar to these.

[2] Note that the IMF simulation for GDP shows the effects on global growth, not the advanced economies, which may be slightly different.

[3] Some forecasters may not expect the oil shock to persist, as is suggested by the longer end of the oil price curve in the forward market. Others may expect the impact to be dampened by exchange rate changes in the eurozone and Japan

SOURCE://blogs.ft.com/gavyndavies/2014/11/13/large-global-benefits-from-the-2014-oil-shock/#

No comments :

Post a Comment